At the present time, when there seems to be such a

desire on the part of every one to do as much as possible to assist in

ameliorating the condition of those in the humbler ranks of society,—

and as, from some unknown cause, there seems to be an earnest desire to

increase the facilities for enabling the poorer classes to save even

small sums, instead of spending them foolishly, not to say sinfully,—we

have thought that, as the increase in the number of Penny Savings Banks

promises to be an immense boon to the working classes, and as

correspondents have asked information regarding them, it would be well

to give a few hints as to the manner of working these institutions,

shewing that they are so simple that any one with an ordinary knowledge

of numbers and a little order and system, can easily manage them. Very

likely some persons never thought of having anything to do with them,

from having taken up the idea of a bank being some mighty great

establishment. Let them divest themselves of this idea, and let them

look on it as the means of collecting together small savings, and

keeping them safely till they are needed for some useful purpose. Many,

many a small sum is thrown away carelessly, and sometimes for drink, for

no other reason than that it is found lying in the pocket. The first

requisite for success, then, is:—Let perfect confidence be established

between the depositors and those who are to have the care of the money.

This can easily be obtained. Let five or six gentlemen of influence in

the locality sign a letter of guarantee, obliging themselves to become

security to the depositors for the safety of their money; they will

incur very little risk by so doing, as they can protect themselves by

keeping a strict watch over their agent or clerk; and for this purpose

the money should be deposited, as soon as convenient, in the nearest

bank—if a branch of the National Security Savings Bank, so much the

better, as they are most accommodating and obliging to the smaller

establishments. Let one of the trustees of the small bank take upon

himself the responsibility of examining the pass-book of the larger bank

every week, to make sure that the money has been paid in, and in this

way not more than the amount collected on one night could be lost, even

supposing the clerk should turn out to be dishonest. Another very proper

precaution is to make the orders for money to be drawn from the larger

bank only payable when signed by the clerk and one of the trustees. The

only books that are required are a ledger and cash-book, which vary in

size according to the prospect of a large or small amount of business

being done. The cash-book may be of the simplest form possible, all that

is required being a column for the number of the deposit and the

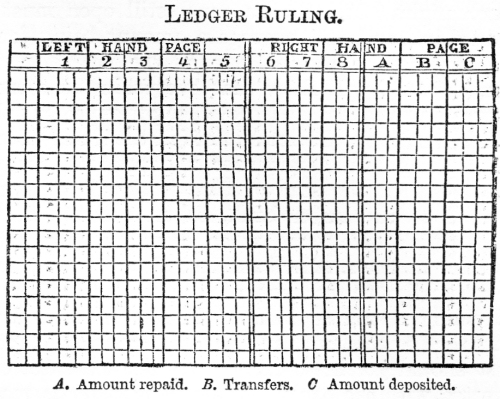

ordinary money column. A very simple form of ledger is the

following:—The two first columns being for the date, we have then eight

accounts, or any number according to the size required, usually twenty

in the two pages, and three additional columns,—the first being intended

for repayments, the second for transfers, and the third for the total

sums received on each night.

The name of the depositor is written on the top line,

and a progressive number, corresponding to the number on the depositor's

book, is carried throughout the whole ledger. The sums deposited and

repaid are entered under their respective numbers, and, at the close of

the transactions for the night, they are added across and filled into

the outer columns. It is quite evident, then, that when the additions of

the outer columns are put together, they must agree with the cash and

also the cash-book, provided they have been correctly posted. By having

the ledger made long enough, twenty-six lines may be introduced from top

to bottom, which, supposing the bank to be open during one night in the

week, will last for six months. Each depositor is furnished with a small

book, in which are inserted the sums paid in on each night, till a part

of the money is to be drawn out, when the different sums are added

together, the amount of the repayment is entered, and deducted so as to

shew the balance remaining. It is not thought advisable to write the

name of the depositor in the small book, as, independently of the great

saving of labour, this plan has been found useful in cases where books

have been lost and presented by the finder, who could not get the money

from not being able to tell the name, shewing plainly that it belonged

to some one else. After the first expense of the ledger and cash-book

has been got over, and a supply of small deposit-books and hand-bills

procured, the current expenses may be very small indeed — a hall, or

school-room, or session-house can easily be procured, and a small sum

will pay for coal and gas; but there is one item of expenditure, which,

after the experience of several years, we believe cannot well be

dispensed with, viz., a small allowance to a clerk, who will take the

entire charge of the ledger. Gratuitous assistance in this matter is

generally freely offered; but our experience has taught us that paid

services only can be relied on for any length of time. Many a young man

would willingly undertake the duty for L.5, 5s. a-year, which is not too

much for two or three hours' attendance for one night in each week,

besides balancing the ledger twice in the year. The clerk should be

assisted by other parties, who will attend in rotation, and give their

services gratuitously, to take charge of the cash-book, as he should

confine his attention entirely to the ledger. The ledger should be

balanced at the end of every six months, to make sure that the accounts

are all quite right. This is a very simple matter, if care has been

taken to make the entries correctly on each night. All the accounts

still open must be added up, and the aggregate amount being found to

agree with the balance at the credit in the larger bank, will shew that

everything is correct. For many reasons, it is not thought expedient

that a large sum should accumulate in the Penny Bank. To obviate this,

whenever a depositor's account has reached the sum of 20s., it should be

transferred to the larger bank, to an account in the depositor's own

name, when he will receive interest for it, the smaller bank not

allowing any interest, partly on account of the useless labour of

dividing a trifling sum of interest over a large number of accounts, and

partly because the interest should go, in so far, to pay the expenses

connected with the bank. When a transfer is made, the pound is deducted

from the sum at the credit, the balance is brought down, and the pound

is entered in the second last column in the ledger headed "Transfers."

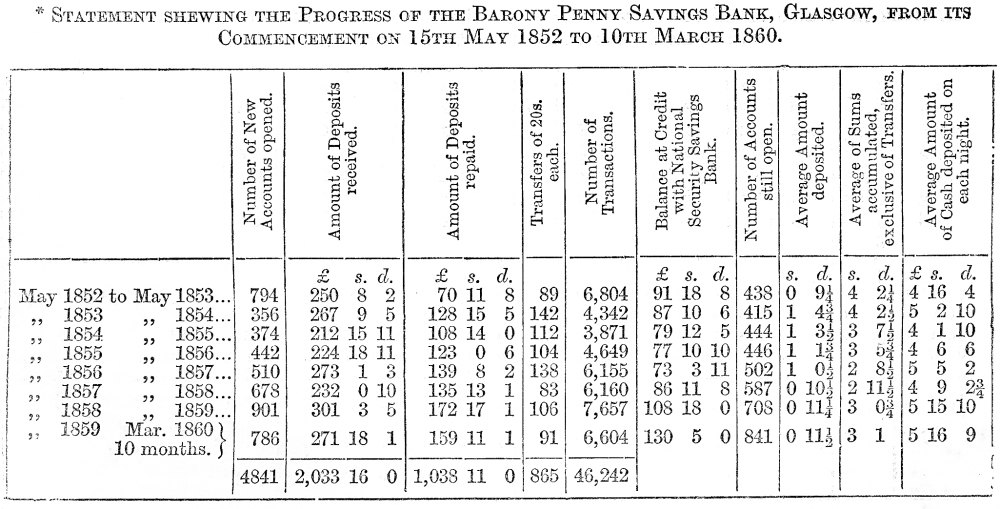

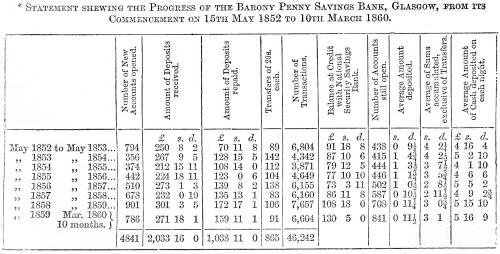

The large sums which have been accumulated in these small establishments

would astonish those who have not had their attention turned to this

matter; in some cases, from L. 15 to L.20, and in many cases, L.6, L.7,

and L.8 have been transferred in the course of a year or two. One of the

Penny Banks in Glasgow has, since May 1852, received in small

deposits—from 1d. upwards—no less a sum than L.2030.

* That they have been productive of a vast amount of good there

can be no doubt, as the gratitude evinced by those who have been

benefited by them is a convincing proof; and, unlike most institutions,

we are not aware that any bad results can be traced to them. There are

some persons—fortunately they are very few in number—who object to these

Small Savings Banks. They may suppose that they have good reasons for

doing so; but we would advise them to look in on a Saturday night at any

of them in full operation, and see the crowd of happy faces of the

depositors; or if they could see, as we have seen, the mother with tears

in her eyes drawing out her money because there was "trouble in the

house," thanking God that she had still something left to carry her

through, and then, before leaving, turning to the bank manager and

saying, "Oh, sir, if it had not been for you I would not have had a

penny," surely they would change their minds, and lend a helping hand to

these institutions, instead of damping the spirits of the promoters of

them. Prom what has been said, it will be seen that the right conducting

of a Penny Bank is a more simple matter than might at first be imagined;

regularity and a correct system, however, being absolutely necessary;

but where these are brought into play, with full confidence on the part

of the depositors in the honour and honesty of those engaged in the

work, success is very certain. A prejudice exists in some minds among

the working classes against these banks, because they suppose that, from

the circumstance of their masters being connected with the bank as

trustees, they have an opportunity of seeing how much money the

depositors are able to save, and may endeavour to lower their wages.

This is altogether a very mistaken idea, and one that no master would

for one moment think of acting on; so much is the reverse the case, that

we venture to say, that there is not a master of any of our public works

who would not rejoice to see all the men and women in his employment

having their bank books; and, so far from reducing their wages, it would

give them a far better opinion of their workers than if they knew that

all their wages were spent and no part of them saved. It must be well

known to many of our readers, that one of our wealthy manufacturers, not

long ago, requested his workers to shew him their savings-bank books;

most of them complied with his request, a few hung back and did not

gratify him. The result was, that he exactly doubled the amount at the

credit of each depositor who had the confidence to shew his book. The

depositors may rest assured that the state of each depositor's account

is kept strictly secret, and is not divulged to any one for any reason

whatever. It would be well

that they dismiss this prejudice from their minds, as

it has no good foundation to rest on. One word of advice to those who

purpose setting up a Penny Bank. Do not be discouraged if, after a time,

say six months or so, you find that the deposits are falling off; this

is very generally the case, but by and by they will increase in number

and amount; in fact, the receipts will ebb and flow, and the bank should

not be allowed to go down because for a time it has not been encouraged

as might have been expected; take courage and carry on, and by and by,

when better known, it will gain new strength and increase. A good plan

is to circulate hand-bills through the houses, reminding the inmates

that the bank is open; let them contain a short address on the

advantages of saving habits, few will take the trouble to read a long

bill.