|

IN the spring of 1837 the Society sustained the loss of

their actuary, Patrick Cockburn, the last survivor of the little band who

founded the Scottish Widows' Fund twenty-three years previously.

3rd January 1839.—Mr. John M'Kean, Manager, died, having discharged the

duties of that onerous office since 1817, two years after the foundation

of the Society. The directors awarded an annuity of £300 to his widow for

21 years, with proportionate provision after her death for such of the

four daughters as should still remain unmarried. They also paid a sum of

£600 to Mrs. M'Kean for her immediate expenses.

Mr. John

Mackenzie, accountant, was appointed Manager in place of Mr. M'Kean,

deceased.

5th April.-No. 7 Pall Mall East was secured as

premises for the Society's agency in London.

In 1847 a

slight flutter may have been caused in the dovecot in St. Andrew Square by

the issue of a prospectus by a company in London calling itself the

English Widows' Fund and General Life Assurance Association. Obviously,

the promoters of this concern calculated on attracting confidence through

the similarity of the title adopted to that of the Society which had

attained a place in the foremost rank of life offices. But the similarity

did not extend beyond the title ; the English Widows' was a proprietary

concern, with an authorised capital of £200,000; and the scale of its

transactions was so insignificant that the wits of the Stock Exchange

dubbed it "the Widows' Mite." In i88 the English Widows' absorbed the

Commercial Life, and in 1860 the combined concern was disposed of to the

British Nation Office, which, finding itself in difficulties in 1865, sold

itself to the European, and the shareholders of both the smaller concerns

were involved in loss by the discreditable failure of the European in

1869.

6th April.-"Resolved that the Right Hon. the Earl

of Rosebery, K.T., be respectfully requested to sit to Mr. Watson Gordon,

artist, for his lordship's portrait, to be hung up in the Convening Room

of the Directors, in grateful and lasting remembrance of his lordship's

unremitting patronage and valuable services to the Society as its

President ever since the foundation of the Institution."

The portrait appears as frontispiece to this volume.

7th

November.-The Extraordinary Court resolved that persons insuring might

commute entry money into an equivalent addition to annual premiums, which

practice is now universal.

1st February 1848.—A captain

in the Royal Navy, insured for £5000, was charged £10 per cent extra on

that sum for service on the coast of Africa.

26th

February i85o.—The Extraordinary Court of Directors resolved that, "in

consequence of the very general feeling of distrust and apprehension

experienced within the last year or two in regard to the management and

direction of many public companies and societies in this country, and in

consequence of the depreciation which it is well known has taken place in

nearly every description of property, we consider it right to take steps

for the purpose of satisfying the Members as to the Situation of this

Society. Although, therefore, it is scarcely two years and a half since a

thorough investigation into •the Society's securities has been made by a

Committee of the Ordinary Court of Directors, . .it is resolved that a

full and complete investigation shall be made by neutral parties,

unconnected in any way with the management and direction of the Society."

It was also resolved that the investigation should apply, not only to the

existing state of the securities, but to the past history of investments

(including loans to members), in order to ascertain what loss, if any, had

been sustained by the Society since its foundation, and whether the loans

on policies had in any instance exceeded the amount authorised by the

Articles of Constitution. The enquiry was also to include the systems of

book-keeping, checks, and audit.

At a subsequent meeting

on 23rd March the following gentlemen were appointed to conduct the

investigation : Mr. James Brown, accountant; Mr. James M. Melville, W.S. ;

Mr. William Brand, secretary to the Union Bank.

The

investigators repo,rted on ioth November. The accumulated fund of the

Society at 31St December 1849 was stated at £2,167,506 9 :1. The report on

this head was to the effect that the whole had been prudently invested,

and that, in the aggregate, the value was in excess of that shown in the

balance-sheet.

The only loss ever sustained by the

Society was found to be a sum of £220, written off the value of a house in

Edinburgh, taken in 1819 as security for £700. This house, having become

the property of the Society in 1845, had been written down to the value of

£480, on which sum it returned a net revenue of 6 per cent.

In three cases, in 1823, 1834, and 1837, it was found that loans had been

inadvertently made on policies slightly in excess of their actual value;

but that excess, in the aggregate, only amounted to £138 : 11 : 8,

and was soon covered by the growing value of the policies.

In short, with a single exception, the tenor of the report was : "Go on as

you are."

The exception was an important one as follows:

Though the books and documents, and the state of business in the office,

afford the most conclusive evidence of the efficiency of the management,

there does appear to the reporters to be a desideratum in the want of a

Secretary—an ostensibly responsible officer, fitted both to communicate

with the public and to assist the Manager in the discharge of his

laborious duties. The use of such a name, even, is reckoned of importance,

for the public are accustomed to it in all great establishments, and they

will not be satisfied with an inferior officer, however meritorious; while

it is physically impossible that the Manager, in his own proper person,

can overtake all the duties which he might wish to discharge, and which

ought to be performed by a superior officer constantly at hand.

Unknown to the authors of the report, the directors had for some time

decided on the appointment of a secretary, as soon as it could be done

without disturbing the flow of promotion. A fitting opportunity occurred

while the investigation was proceeding through the death of Mr. George,

head clerk, and Mr. William Lindesay, accountant, was appointed secretary.

5th February 1856.—Hitherto it had been the rule that in the event of an

insured person dying on the high seas, his policy should be void. This

rule was now repealed so far as such deaths should occur in European

waters, as affecting prior, existing, and future policies.

26th April 1859.—The bye-law under which extra premiums were charged on

bonus additions to policies as well as on the sums originally assured, was

repealed.

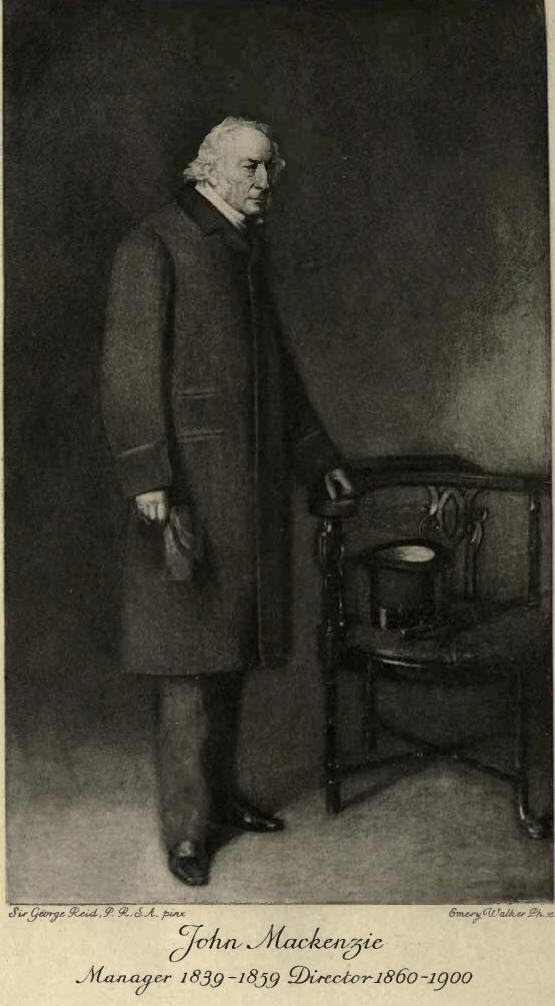

3rd May.-The Court express their extreme

regret caused by the resignation of -the Manager, Mr. Mackenzie, after

twenty years' excellent service, at the same time congratulating him

cordially on "the unsought and highly honourable distinction conferred

upon him." He had been appointed Treasurer of the Bank of Scotland, an

office which he only held for a single year, owing to a breakdown in

health. He was, however, elected a director of the Society, and the Court

also directed that Soo guineas be presented to him "in such form as he may

prefer, as a suitable memorial of their high approval of his conduct and

of their sense of the important services rendered by him during, the

period of twenty years for which he has held the office of Manager." Mr.

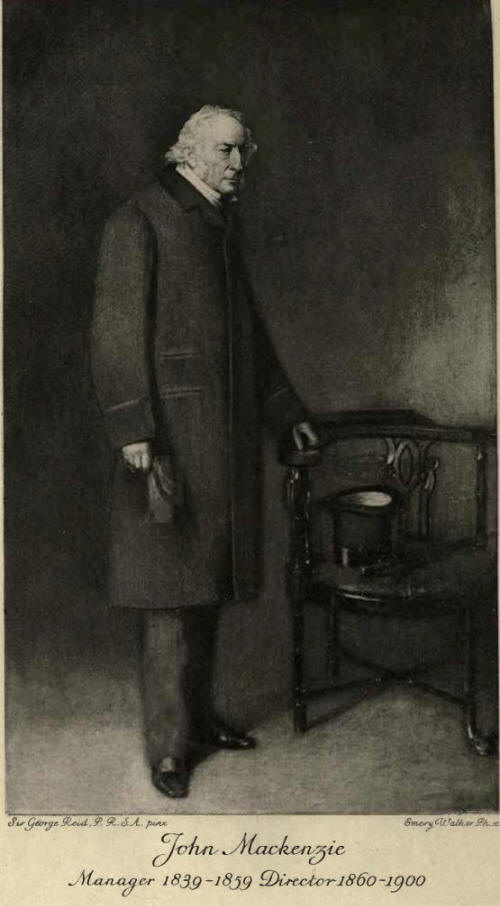

Mackenzie's tall, lean figure and handsome features were familiar to many

inhabitants of Edinburgh. His portrait, painted by the late Sir George

Reid, hangs in the Convening Room [That is the old-fashioned name of the

Board Room.] of the directors, and is reproduced in Plate opposite.

17th. - Mr. Samuel Raleigh, chartered accountant, was appointed Manager in

succession to Mr. Mackenzie, resigned.

In this year,

1859, the Society purchased 9 St. Andrew Square, the premises occupied at

the present day, from the liquidators of the Western Bank, for which the

building had been erected in 1857.

28th June 1861.—From

time to time during the existence of the Society resolutions had been

proposed, considered, and decision upon them deferred (for one reason or

another), that a petition should be presented for a charter of

incorporation. A Bill for that purpose having been now introduced in

Parliament, it passed through both Houses unopposed, and received the

Royal Assent on this date.

27th May 1862.—The limit of

assurance upon a single life was raised to £10,000.

25th

April 1864.—From its foundation in 1815 the Society's operations had been

conducted on the basis of the Northampton Tables of Mortality, calculating

the rate of interest at 4. per cent. It was now resolved to substitute at

the end of the current year the Carlisle Tables, calculating interest at 3

per cent.

1st November.-The rate of interest on loans

made by the Society upon the security of heritable property or on that of

their own policies was raised to 4 1/2 per cent.

At the

septennial investigation of 1866 the attention of members was drawn to the

increase in the number of agencies. In the early years of the Society the

bulk of the business came unsolicited, and little or no commission was

paid ; but most of the old policies had lapsed through death of the

insured, and the transactions of the Society now extended far beyond the

radius of personal influence on the part of directors and their friends.

Consequently, in view of the keen and ever-increasing competition of rival

offices, it had become necessary for the Society, in order to keep the

high position it had attained, to add largely to the number of its agents.

During the septennium ending 31st December 1859 the agents had not

exceeded 120; at 31st December 1866 they had been increased to 400, and,

in addition to the branch offices long established in London, Manchester,

and Glasgow, similar offices had been opened in Dublin, Leeds, Liverpool,

Belfast, Birmingham, and Dundee.

This caused a

considerable increase in the expenses of management at the Head Office and

agencies, which, during the septennium 1852-59, had never exceeded 4 1/4

per cent of the revenue, a lower rate, probably, than any contemporary

Life Offices could show. At the investigation of 1866 these expenses were

found to have risen to 6 1/4 per cent ; but it was also shown that the

ratio borne by the expenses of management to the first premiums of new

assurances was, at the close of the septennium 1859-66, just one-half what

it was at the beginning of the septennium. The additional cost, therefore,

was fully justified by the volume of new business secured.

Since 1866 the Society's business has continued to show a large increase.

Thus, while in the seven years 1860-66 new policies were issued to the

number of 8112, assuring £5,461,884—or an average business of 1159

policies for £780,269 per annum—the new policies issued during the five

years 1909-13 numbered 21,069, for £12,587,123, after deduction of sums

reassured, or an average of 4214 policies for £2,517,424 per annum.

The expenses of management stand now as they did fifty years ago, at about

10 1/2 per cent on the premium revenue, which is considerably below the

average of insurance offices in the United Kingdom, as shown in the

returns published by the Board of Trade. The difference or saving goes to

swell the amount to be divided as bonus among the policyholders.

In 1866 the field of investment was extended by the directors to Ireland,

and they continued to advance loans upon the security of mortgages on land

in that country until 1880. In that year, having regard to the trend of

legislation affecting Irish land, it was decided that this was no longer a

desirable subject for investment, that no more loans should be made on

that class of security, and that those outstanding should be gradually

called in. The amount outstanding in that year was £1,204,100 ; before the

end of 1894 £846,560 had been repaid, leaving a balance of £357,44.0,

which was then and there written down to £302,000. In the end the

investment did not prove to have been unprofitable, owing to the high rate

of interest obtained on Irish mortgages, which averaged £4: 6 10.

The disastrous failure of the Albert and European Life Offices seriously

affected the business of other London offices for a time, but its effect

was hardly perceptible in the affairs of the Scottish Widows' Fund. As a

consequence of the aforesaid failures the Government introduced and passed

the Life Assurance Companies Act of 1870 (33 & 34 Vict. cap. 61),

requiring every Company to publish annual accounts, to hold periodical

investigations, and to furnish policyholders and shareholders with

actuarial reports on demand. No additional burden was laid on the

directors and manager of the Scottish Widows' Fund by this legislation,

inasmuch as it had been their established practice to publish

balance-sheets and valuations, and "the Summary and Valuation of Policies"

required by the Act was substantially the same as that given in the

septennial reports to members. Moreover, the greater publicity given to

these particulars by their issue from the Board of Trade enabled persons

contemplating insurance to realise the strength of the Scottish Widows'

Fund, with the result that new business increased at a rate exceeding

anything in the experience of the management.

10th

December 1880. - A Special General Court was held on this day, when

several important modifications in the laws of the Society were passed

unanimously.

1. The rule requiring that none but a

person residing in the County of Edinburgh should be eligible as an

Ordinary Director was repealed.

2. The Carlisle tables,

with interest calculated at 3 per cent, were discontinued as the basis of

the Society, and the Tables published by the Institute of Actuaries, with

interest calculated at 3 1/2 per cent, were adopted instead.

3. The Guarantee Fund, which was constituted under a bye-law of 29th

December 1864, in consequence of the Carlisle Tables assigning a value to

advanced life higher than accorded with the experience of the Society, was

discontinued.

9th February 1882.- A Special General

Court approved of "a Bill to consolidate and amend the Constitution and

Articles and Regulations of the Scottish Widows' Fund Life Assurance

Society, to confer further powers on that Society, and for other

purposes."

In moving that the Bill be introduced into

Parliament the Chairman of the Court, Mr. John Gillespie, W.S., observed:

It says a good deal for the forethought and skill of those who devised the

original laws and constitution of our Society, that those following them

in the administration of its affairs have with such success been able to

rear upon those foundations so splendid an edifice. But a great deal has

happened since 1814. The conditions of life in many respects have altered.

Men are now in the habit of going to distant countries much more

frequently than they did. . . . It is desirable that these and other

altered conditions should be provided for. . . . The volume which contains

your rules and regulations has become a very large one indeed. Even a

person well accustomed and versed in the affairs of the Society has great

difficulty in knowing precisely where to find the precise law upon

particular points; while an inexperienced person, I am afraid, would in

many instances not be able to find what he wanted at all. It therefore

seemed to us most desirable, if not absolutely necessary, that those rules

and regulations should be consolidated. . . . Our custom hitherto has been

not to pay claims until six months after the death of the policyholder . .

. the custom of earlier payment of claims has become almost universal with

other offices . . . the Directors have therefore thought it right in this

Bill now before Parliament to take power to shorten these periods.

Subsequently, at the Sixty-ninth Annual General Court, Mr. Gillespie said

that the earlier payment of claims had been very frequently urged upon the

directors by some of the members, who had not, perhaps, duly understood

the effect upon the Society's funds. He now explained that shortening the

period for payment of claims from six months to three would cause a

corresponding reduction in the Society's revenue amounting, at the end of

the septennial period, to £45,000, arising from sacrifice of interest.

For more than half a century the bulk of the Society's funds was invested

in mortgages upon Scottish land, and, later, in those on land in England.

The extension to Irish mortgages in 1866 has been noticed already. No loss

whatever had been sustained upon Scottish and English mortgages, owing to

the care taken in maintaining an ample margin in value. But the supply of

securities on land was limited, it had been heavily invaded by other Life

Offices, whereof the number had been constantly increasing. Consequently,

in 1896 power was taken by the Society to invest in foreign and colonial

securities, an office having already been opened in Sydney in 1886 for

effecting loans. Twenty years later this office was closed, in consequence

of the credit of Australian borrowers having so improved as to enable them

to obtain loans at the same rates as were current in the mother country.

There was, in consequence, no advantage to be obtained in keeping a loan

office at the Antipodes.

28th September 1906.—The limit

of risk on a single life was raised to £20,000, and the maximum for

annuities to £2000.

During the septennium 1888-94 the practice of the Society was modified in

three important particulars, each of which affected beneficially the

interests of policyholders.

1. Earlier Settlement of

Claims.—In 1890 the Court decreed that claims should be made payable at

once on proof of death, or other contingency insured against, and title to

claim, being produced, instead of payment being delayed for three months.

2. Power to surrender Intermediate Bonus.—In 1891 the Society obtained an

Act of Parliament legalising dealings with intermediate bonus, which had

hitherto been debarred.

3. Payment of Estate Duty. - In

1893 the Court decreed that the representatives of an insured person

deceased might have the sum payable under his policy, or any part thereof,

applied to the payment of Estate duty, before issue of a grant of

representation.

28th September 1906.—Members, not being

sea-faring persons, were allowed to reside or travel in any part of the

world, Asia excepted, north of 33° north latitude and south of 30° south

latitude, and in the treaty ports of China, without extra premium. |