|

IT was in the midst of

the experiences described in the last chapter that the earliest of

Scottish banks came into existence, and passed the first few years of

its career. On the 17th July 1695, three weeks after the incorporation

of the African and Indian Company, the Scots Parliament passed an "Act

for erecting a Publick Bank," [The quotations are from a print dated

1695.] which, together with six other Acts subsequently obtained, forms

the constitution of the Bank of Scotland. The preamble recites how " Our

Soveraign Lord, considering how useful a Publick Bank may be in this

Kingdom, according to the custom of other Kingdoms and States; and that

the same can only be best set forth and managed by Persons in Company

with a Joynt Stock, sufficiently indued with these Powers, and

Authorities, and Liberties, necessary and usual in such Cases; Hath

therefore Allowed, and, with the Advice and Consent of the Estates of

Parliament, Allows a Joynt Stock, amounting to the Sum of Twelve Hundred

Thousand Pounds [Scots] Money, to be raised by the Company hereby

Established for the Carrying and Managing of a Publick Bank. And further

Statutes and Ordains, with Advice foresaid, That "certain persons named

should have power to receive subscriptions from the 1st November to the

1st January succeeding, and that the subscribers "are hereby Declared to

be One Body Corporat and Politick, by the Name of the Governour and

Company of the Bank of Scotland."

After sundry provisions

regarding the election of office-bearers, and the general management of

the bank, and other matters, it is enacted that during the space of

twenty-one years "the Joynt Stock of the said Bank continuing in Money,

shall be free from all Publick Burden to be imposed upon Money," and "it

shall not be Leasom to any other Persons to enter into and set up an

distinct Company of Bank within this Kingdom, besides these Persons

allenarly in whose Favours this Act is granted." That the bank would

issue notes was recognised, without specification of powers, by the

provision "And sicklike, it is hereby Declared, that summar Execution by

Horning, shall proceed upon Bills or Tickets drawn upon, or granted by,

or to, and in Favours of this Bank."

They were debarred from

any "other Commerce, Traffick, or Trade with the Joynt Stock ... or

Profits arising therefrae, excepting the Trade of Lending and Borrowing

Money upon Interest, and Negotiating Bills of Exchange allenarly and no

other," and from lending to or otherwise financially assisting the

Crown, except where "a Credit of Loan shall happen to be granted by Act

of Parliament allenarly." The Act concludes with the provision " that

all Forraigners, who shall joyn as Partners of this Bank, shall thereby

be and become Naturalised Scots-men, to all Intents and Purposes

whatsoever."

Among the names mentioned

in the Act are several which also appear in the African and Indian

Company's Act; but there is one notable exception.' Seven London

merchants are included in the list, of whom the names of John Holland

and Thomas Coutts are specially interesting. But William Paterson, the

founder of the Bank of England, the foremost Scotsman of the time in the

domain of finance, he who, according to a contemporary poet, could

"persuade a nation bred to war to think of trade," is too busy leading

his countrymen on a will-o'-the-wisp chase to interest himself in a

matter which far more concerned his country's good than all his dreams

of foreign wealth. He even appears to have viewed the banking project

with disfavour, but for what reason is not apparent.

To whom the credit for

the original idea of a bank in Scotland is due seems unascertainable;

but it is understood that Mr. John Holland, whose name is inserted in

the Act, a merchant in London, drew up its constitution at the request

of several Scotchmen resident in London. At the outset, the governor and

one-half of the directors were elected from among the proprietors

resident in London, the deputy-governor and the other half of the board

being chosen from among the Scottish proprietors. Mr. Holland was the

first governor. Subsequently, from want of interest in the bank leading

to a gradual decrease in the number of English proprietors, the practice

of electing London directors was abandoned. Mr. Wenley says: "It would

appear that Mr. Holland's Scotch bank had not found much favour with his

English friends; but there can be no doubt that, under his care, it had

been judiciously planted, and had fairly taken root." [Journal of

Institute of Bankers, vol. iii. p. 121.]

Although, as we have

seen, the Bank of Scotland got its credentials on 17th July 1695, it was

not until the new year that the share-subscriptions were completed, and

the bank actually commenced business. The capital was subscribed for in

the proportions of two-thirds in Scotland and one-third in London. The

payments on application for stock, amounting to £10,000 sterling, or 10

per cent of the subscribed capital, sufficed for the bank's

requirements. They began at once to issue notes of £100, £50, £20, £10,

and £5 sterling; and in 1704 they adopted a £12 Scots (value £1

sterling) denomination. It is somewhat extraordinary that, at the

outset, the notes should not only have been in English currency, but of

such high denominations. The number of people who could have had use for

the larger of these amounts must have been very small; and even £5 would

be an unattainable sum for most of the population. The explanation is,

doubtless, as suggested in the letter referred to below, [It is stated

in the Historical Account that, in January 1699, they adopted a 20s.

issue. The author subsequently, however, enumerates only the first five

denominations as current in 1700; and his statement is otherwise

unconfirmed. That it is probably an error is apparent from an

interesting official letter printed in Appendix A. The notes, we are

told, were then "engraven in one and the same character, only the

amounts being different."] that the bank was dominated by the views of

people accustomed to the conditions of business in London. Hence also

the hesitation of the bank, until 1704, to issue small notes, which were

essential to the efficiency of the circulation.

At first the lending of

their capital and the issue of notes constituted the whole of their

business, but very soon they attempted to engage in exchange business,

for we find that in this first year of their active existence (1696)

they established branches at Glasgow, Aberdeen, Dundee, and Montrose. It

is possible that the immediate cause of this movement was an attempt

made by the African and Indian Company to engage in the business of

banking, as a set-off to their failure in Darien, and the unremunerative

nature of their other commercial ventures. This action was, of course, a

direct infringement of the legal monopoly of the bank, justifiable only

by a literal interpretation of the prohibitory clause of the bank's Act,

which forbade the setting up of "a distinct company of bank." Not

feeling themselves strong enough, however, to contest the point, the

bank allowed their opponents to carry on their competition undisturbed;

and very soon it was found that the latter were as unable to command

success in banking as in their legitimate business, and they retired

from the field. "They resolved," says our author, "not to quarrel with

that (then) Mighty Company, nor plead the Bank's seclusive Privilege;

but rather to ly by for a little, and only so to manage their Affairs,

as not to suffer an Affront in their Infancy, by a Demand on the Bank

greater than the Amount of their Cash: And this they did effectually,

but with some Loss to the Company; for it obliged the Proprietors to

advance two Tenths of their Stock, besides the Tenth paid in at

subscribing, and put a stop to all Negotiations for a Time" (p. 4). In

the year succeeding the establishment of the bank's branches, the

directors, finding [Parliamentary Report, 1841.] that the expense of

conducting them greatly exceeded the profit obtained, withdrew them, and

the attempt was not renewed during the currency of their monopoly. To

meet their extended operations they had increased the paid-up capital to

£30,000; but when they again confined their business to Edinburgh, it

was reduced (May 1698) to the former amount by repayment of £20,000 to

the proprietors.

In February of the year

1700, they had the misfortune to be burned out of their office, which

was situated in Parliament Close, but, while the event occasioned alarm

and inconvenience at the time, they do not seem to have sustained much

injury therefrom. It was not long, however, before their affairs assumed

a grave aspect. The issue of notes had doubtless proved a great boon to

the public, as well as a source of profit to the bank, but the use of

them was not at this time so general as it afterwards became. As an

addition to the currency they were acceptable; but coin was still the

recognised medium. In 1704 a scarcity of coin, occasioned by a

persistent drain of bullion (probably to meet the foreign payments of

England in connection with the wars under Marlborough, who gained his

great victory over the French at Blenheim in August of this year), began

to be severely felt. A rumour "that the Privy Council was to cry up the

value of species," as it was quaintly termed, brought matters to a

crisis with the bank. In the words of an official print, dated 28th

December 1704, and styled a "Memorial and Intimation from the Governour

and Coy. of the Bank of Scotland," these circumstances "occasioned a

very great, unexpected, and unaccustomed demand upon the bank, which at

last had such effect, that on Munday the 18th of this instant December

the money in the Bank was wholly exhausted, and thereby payments stopt."

Thus, in language contrasting strangely with the euphonious circulars in

which firms now announce their inability to meet the demands of

creditors, did the directors of the Bank of Scotland intimate that they

had suspended payment.

Confident, however, in

the perfect solvency of the corporation, they proceeded to state that

application had been made to the Marquis of Tweeddale, the Lord High

Chancellor, craving an inspection of the books. Thereupon the Earl of

Loudoun, Lord Belhaven, the Lord President of the Court of Session, and

others, met at the bank, and after examination they "find that the Bank

hath sufficient Provisions to satisfie and pay all their outstanding

Bills and Debts; and that with a considerable Overplus, exceeding (by a

fourth part at least) the whole foresaid Bills and Debts." A general

meeting of the adventurers was called, who sanctioned the allowing of

"annual rent" on the notes "from the stop," to procure their continued

currency, and made a call of 10 per cent on the nominal capital,

amounting to £10,000. This sum was repaid two years later. With these

arrangements the difficulty was overcome, and the bank learnt its first

lesson in the absolute necessity of maintaining an efficient bullion

reserve. It had probably been loth to supplement its falling stock,

owing to the great expense attending such an operation. This will be

readily understood, when it is remembered that the cost of bringing gold

from London amounted then to 8 per cent or 9 per cent on the remittance.

The year 1704 is further noticeable, from the first step in the

establishment of the small-note currency, which subsequently proved such

an important factor, having been taken, by the bank then commencing the

issue of notes of the value of £1 sterling. Their circulation was,

however, very limited until after the union of the countries.

Three years after the

incident we have just narrated (1st May 1707), the legislative union of

England and Scotland was accomplished, after protracted and acrimonious

negotiation. That event is now regarded as a mutual blessing to both

nations; but it was not generally so considered at the time. Haughty and

contemptuous, the English looked on it as a means of staving off the

troublesome incursions of the northern wolves. The Scotch, on the other

hand, detested the proposition, and but for intrigue and bribery among

the members of Parliament, the Act of Union would not have passed. The

people were not, however, long in finding out the material benefits

accruing to them from federal union with their wealthy neighbours, and

from that time Scotland rapidly advanced in civilisation and commerce.

The national coinage being then in a very unsatisfactory condition, the

Bank of Scotland was entrusted with the duty of superintending its

improvement. "The Directors undertook to receive in all the Species that

were to be recoined, . . . and to issue Bank-notes or current Money for

the same, in the Option of the Ingiver of the old Species, and the Privy

Council allowed a Half per Cent, to the Bank for defraying Charges." The

bank were promised a reward after finishing the work; but, although they

preferred their claim, they do not seem to have secured its recognition.

[Historical Account of the Bank of Scotland, 1728.] The total metallic

currency of Scotland at that time has been estimated at £800,000, or,

according to one authority, £900,000. Of this, £411,117 : 10 : 9 was

brought in, in exchange for new coin. It is interesting to note that

only £239,636: 13 : 9 was native coin, the rest consisting of £132,080:

17s. of foreign and about £40,000 English coin. This operation took

place in 1707.

While this reform was in

progress, the bank got a great fright; "For in March 1708 the French

Fleet appeared at the mouth of the Firth of Forth, in the (then)

intended Invasion. At which time the Bank had a very great Sum lying in

the Mint in Ingots, and a considerable Sum in the Bank, brought in to be

recoined, besides a large Sum in current Species; all which could not

well have been carried off and concealed." [Ibid.] In 1707 the bank

first assumed the role of a bank of deposit, but did not then allow

interest on the money paid in. During the Jacobite troubles of 1715 the

bank, being suspected of favouring the Pretender's cause, fell into

disfavour with the Crown. To this is ascribed the favourable reception,

some years afterwards, of the request by the Equivalent Company to have

banking powers conferred on them, and the special recognition and

support accorded to them for long afterwards as the great rival of the

Bank of Scotland.

It does not concern us to

trace the course of the rebellion, which, indeed, does not seem

materially to have affected the country in general. But it is

interesting to observe its effects on the bank. That establishment,

despite the insignificance of its financial position from a modern point

of view, appears to have been a considerable power in the land. It would

appear that its influence was (doubtless secretly) enlisted more in the

cause of popular patriotism (according to the light of those days) than

in the interest of public order and loyalty, as these were regarded by

the dominant party. For this disaffection to King George the bank was

severely punished twelve years later; and even at the time it suffered

from the results of the rebels' action. The Town Council of Edinburgh

made successful endeavours to provide for the security of the city; but

the approach of a detachment of the Pretender's party produced so much

alarm among the citizens, that a severe run on the bank took place. It

is recorded that "the enterprise began on the part of the rebels with an

unsuccessful attempt to seize the Castle by surprise and the run on the

Bank of Scotland was so great, that they stopped payment on the 19th

September [having apparently sustained it for eleven days], and ordered

their notes to bear interest from that date." Elsewhere, however, we are

informed that "the Directors privately encouraged the Demand, lest the

Money should fall into the Hands of Enemies. But the Directors took Care

to retain the whole Cash belonging to the Government; and after all the

rest of the Money in the Bank was issued, they delivered the publick

Money; which was lodged in the Castle of Edinburgh, being about £30,000

Sterl." Tranquillity was restored by the arrival of troops from Holland

in December following. The interest-bearing notes were withdrawn from

circulation during May, June, and July 1716, "and the Directors

proceeded again in Business and Negotiations." [Historical Account.]

In that year, as the

result in all probability of the interruption of its business, it does

not appear to have paid any dividend. As this was quite an unusual

circumstance, even in those early days of the bank's history (as far as

we are aware it occurred only once before and never after), and as, when

dividends were resumed, they were at lower rates than those immediately

preceding the cessation, it would seem that the bank had suffered

considerably from the untoward train of events. The proprietors could,

nevertheless, afford to dispense with a year's dividend, seeing their

profits had been of a very substantial character. From an apparently

authentic record we find that, for the twenty-nine years ending with

1727 (the date of the incorporation of the Royal Bank), the allocated

profits averaged 17 per cent on the capital. After the first stoppage

(1704) the rate fell to 6 per cent, but it was rapidly raised again

until it reached 30 per cent, at which it stood for three years prior to

the second suspension (1715-16). In the succeeding eleven years the rate

varied from 10 per cent to 22 per cent, and the bank enjoyed an

undisturbed and lucrative monopoly. Its exclusive privileges had lapsed

in 1716, but no competitor had arisen to contest its sway in the domain

of finance. Indeed, there are indications that in those days an opinion

prevailed pretty generally that, while one bank was necessary, a

plurality of banks was unadvisable and even dangerous. The great South

Sea Bubble and the other speculative manias which in 1719-20 grievously

afflicted the English nation, appear to have had little effect on

Scotland.

The prosperity of the

Bank of Scotland did not pass unobserved. Although up to 1726 no actual

competition, other than the ineffectual attempt made by the Darien

Company, seems to have been threatened, endeavours were made by other

corporations to share their gains. One of the most curious of these was

a scheme submitted by a Mr. James Armour, writer in Edinburgh, acting on

behalf of the Royal Exchange Assurance Corporation of London. In

advancing his scheme, Mr. Armour lays great stress on the benefit to be

derived by the country from its acceptance; but it is evident from his

tone that he had some strong personal interest in the success of his

proposals. Seemingly the bank directors had turned a deaf ear to his

charming, for he issued a print of 25 pages, with the object of forcing

the scheme upon their attention, and enlisting the support of the

proprietors. This pamphlet is entitled, "Proposals for making the Bank

of Scotland more Useful and Profitable, and for raising the Value of the

Land-Interest of North Britain; Edinburgh, 1722." It is dedicated to the

Earl of Leven, Governor of the Bank, "to whom," says the author, "I'm

perswaded, what is offered with a View to serve your COUNTRY and the

BANK-COMPANY, will not be unacceptable." He then addresses the reader in

the following words:—"Being commissioned by some very Honourable

Gentlemen, as a COMMITTEE of the DIRECTORS of the ROYAL EXCHANGE

ASSURANCE COMPANY at LONDON, to offer the following PROPOSALS to the

GOVERNOR and COMPANY of the BANK of SCOTLAND, which, in my humble

Opinion, are for the Interest, not only of the BANK-COMPANY, but also of

the whole NATION, I think myself obliged to submit THEM to the

consideration of every one who will take the Trouble to examine 'EM, and

has Resolution enough to judge for himself. 'Tis in vain to write for

him, who, for Want of this Resolution, submits himself and his Concerns

to another's Conduct, without enquiring into the Reasons of Things, such

a one may save himself the Trouble of examining these Proposals, and

leave it for a Task to his DIRECTOR." He then devotes sixteen pages (in

which a peculiar taste in printing is gratified to the full by the

liberal use of large and small capitals, italics, and old English

characters) to the statement and advocacy of his proposals. He opens

with a reference to "The bad Effects of the Scarcity of Money, and a

sunk Credit" then existing; and continues, "'Twill be needless for

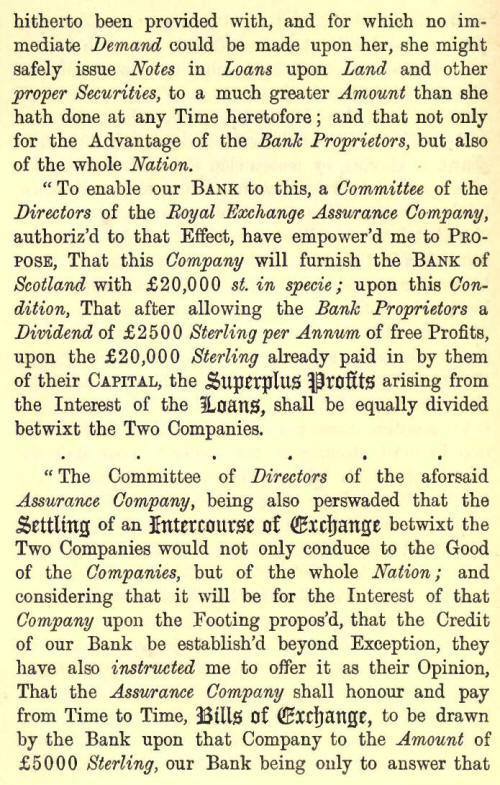

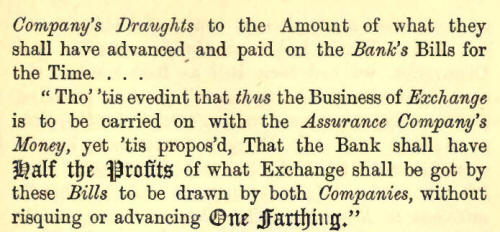

The deposit of £20,000

was to lie for a period of nineteen years, with option to the Assurance

Company to demand repayment on twelve months' notice, but with no option

to the bank to repay of their own accord. As the bank had been paying

dividends of 20 per cent on the first instalment of £10,000 of their

capital, and of 5 per cent on the second instalment of the same amount,

the sum of free profits specified was to preserve that position. Further

profits, including those to be derived from the use of the Assurance

Company's money, were to be divided equally between the bank and the

company. The exchange business was to be kept separate, one per cent

commission to be charged, drafts to be payable at sight, each party to

pay their own expenses, and the profit to be divided equally.

Our author seems to have

had doubts as to the acceptance of his scheme, for, towards the end of

his pamphlet, he expresses himself thus gloomily and sarcastically: "I

know that very often the most useful Proposals" [he has long before this

exhausted his stock of special types] "have been treated with the

greatest Contempt; but a Man that has any Share of good Sense, must

perceive how absurd this conduct is. If the World had been always averse

to new Discoveries, we had been still as Barbarous as the most ignorant

of our Ancestors" [a most profound depth surely], "and sure, one can't

read the Proposals now offer'd with any Degree of Attention, but he must

be ready to think, they will be Accepted with Pleasure, unless" [here

comes the sting] "this is sufficient to Reject them that they are made

feasible, and for the publicic Good." |