It is one of those strange accidents of history that

the four major organisations in Scottish banking should have been

founded in different ways. Since 1695 commercial banking in Scotland has

produced more than 100 banks—of these only three remain—the Bank of

Scotland, Royal Bank of Scotland plc and Clydesdale Bank PLC. Also since

1810 the savings bank movement has produced a similar number of banks

and of these only four remain.

In 1695 an Act of the Scottish Parliament constituted

the Bank of Scotland as a legal entity. This gave it power to sue and be

sued in its own name, and it was also generally agreed that the Act

conferred limited liability upon the shareholders. This meant that if at

any future time the Bank had to be wound up then the shareholders could

not be forced to pay any more than that part of the authorised capital

for which they had subscribed.

The same benefits were obtained by the Royal Bank of

Scotland when it was founded in 1727, but this time the constituting

document was a Royal Charter rather than an Act of Parliament. When the

British Linen Co. (later British Linen Bank) was set up in 1746 it too

was constituted by a Royal Charter. The fact that all three concerns had

limited liability made their shares very attractive to the investing

public because most businesses in the 18th century were organised as

partnerships. The law of partnership meant that any one who invested

money in such an organisation became a member of it and was therefore

liable for all of its debts, i.e., if the business's liabilities

exceeded its assets when it was being wound up then the personal assets

of the partners could be sold to pay the debts of the business.

Not all banks, however, were organised and

constituted in such a way that the benefits of limited liability were

conferred upon them. In fact most of the banks which were founded in the

18th century were partnerships. There were two different kinds of these

banks. Firstly the private banks in Edinburgh of which there were about

twenty, many of which failed in the crisis of 1772. These were mainly

very small non-note issuing banks who borrowed money from the Bank of

Scotland and Royal Bank which they then lent to their own customers at a

slightly higher rate of interest. Very little is known about these

concerns but it does not seem that they were of great significance to

Scottish economic development. Possibly the sole exception to this

generalisation was the house of Sir Wm Forbes, James Hunter and Co.

which grew to some prominence as a deposit gatherer and then began to

issue its own notes in order to further extend its business.

Of much more importance to economic progress were the

provincial banking companies of which forty-five were formed in the

period 1747-1825. These tended to be much larger than the private banks

although smaller than the Bank of Scotland or Royal Bank. They were set

up as partnerships, ranging in size from six to eighty partners, in all

of the larger burghs and some of the smaller ones. By 1800 there were

provincial banking companies in Glasgow, Dundee, Aberdeen, Stirling,

Perth, Ayr, Paisley, Greenock, Falkirk and Leith and others followed in

the 19th century. Many of these concerns were set up before the large

Edinburgh banks had extended their operations to include a branch system

so that when branches were set up they often had to face competition

from one or more of the banking companies. Competition was therefore a

major feature of the evolving Scottish banking system and the result was

a service which was certainly more efficient and probably cheaper than

its English counterpart.

In England the Bank of England had been set up in

1694 largely as a result of the efforts of the Scot William Paterson. It

was not England's first bank as several London goldsmiths had evolved

the banking functions of deposit, note issue and lending earlier in the

17th century. Nevertheless, the Bank of England soon came to dominate

the English banking scene from its London base. An Act of 1708 which was

passed to defend the Bank's monopoly of joint-stock banking in England

and Wales enacted that no other bank in these countries could have more

than six partners. By 1750 there were about twelve country banks in

English provincial areas but all were restricted by the legislation of

1708. The result of this restriction was that England and Wales were

deprived of a system of banking commensurate with a period of rapid

economic growth.

Of course in 1750 the Scottish people were much

poorer than their English counterparts and were very conscious of this

fact. If they were to catch up with their southern neighbours it was

absolutely essential that they develop a system of banking which would

create credit and mobilise savings in as efficient a way as possible. As

we shall see the Scottish banking system, within the British Isles,

pioneered in an extensive way several major developments including

joint-stock organisation, deposit taking with interest, note exchanges,

branch banking and cash credits (the forerunner of overdrafts). Scotland

was very fortunate in that the Government left the system free of

restrictive legislation so that it could develop in line with the

requirements of its customers. The path to the achievement of this

highly effective banking system was not, however, always very smooth.

It is a perfectly natural phenomenon in human

relations that well established individuals will be suspicious of new

arrivals until they either prove that they are not a threat or can be

controlled in some way—and so it is in business; especially when the

rival organisations are constituted differently. In the mid-18th century

the Bank of Scotland and Royal Bank of Scotland, after initial distrust,

had settled into relatively peaceful co-existence. Their peace was

shattered, however, when, from 1747, the provincial banking companies

began to be formed. Initial attempts by the Edinburgh banks to control

these new arrivals failed and a period of considerable hostility ensued

before peace was restored in 1771 when the Edinburgh banks decided to

set up a note exchange and forced the provincial banks (nine in number)

to join. The effect of the exchange—the first of its kind—was to place

proper limits on the amount of notes which a bank could keep in

circulation. From then on banks could only keep in circulation those

notes which their customers required for daily transactions. Other notes

had to be retired, either over the counter or through the exchange.

The following year there occurred one of the worst

commercial crises that Scotland has ever seen. Several of the small

private banks in Edinburgh failed as did Douglas, Heron and Co. (the Ayr

Bank), the largest of the provincial banking companies. The crisis might

have been even more serious had it not been for another innovation,

i.e., the preparedness of the Bank of Scotland, the Royal Bank and,

to some extent, the British Linen Company to act as lenders of last

resort by lending cash to some of the provincial banking companies,

whose business was otherwise sound, but who had problems of providing

adequate liquid assets to meet the demands of their customers. In other

words the Edinburgh bankers were prepared to develop at least some of

the functions nowadays normally associated with a Central Bank.

The willingness of the Edinburgh bankers to act in

this way brought considerable stability and confidence to the Scottish

banking system. Thereafter commercial crises were never experienced with

such intensity as they were in other parts of the British Isles. The

preparedness of the banks to help one another meant that the banks were

better able to help their customers through difficult times. Nowhere was

this more evident than in the crisis of 1825-6 when sixty country banks

in England failed with considerable loss to the public who held notes or

deposits with the failed banks. In Scotland only two of the smaller

provincial banks failed but their difficulties were of long standing.

Despite this there was no loss to the public and all debts were paid in

full. This experience reinforced the writings of Thomas Joplin, a

Newcastle merchant, who had published a pamphlet in 1822 decrying the

English banking system and extolling the virtues of the Scottish banks.

Joplin's arguments were highly polemical and therefore sometimes not

terribly accurate but there was sufficient truth and perceptive comment

in his writings for them to carry a certain amount of political weight.

A Parliamentary enquiry was set up specifically to enquire into the

issue of bank notes in Scotland and Ireland but, more generally, to

enquire into the whole system of banking. The Government planned to

abolish the right of Scottish banks to issue notes under £5—a right

which they had always enjoyed. Such was the clamour from Scotland that

Parliament appointed the committee of enquiry which found that Scottish

banking was—

"a system admirably calculated to economise the

use of Capital to excite and cherish a spirit of useful Enterprise,

and even to promote the moral habits of the people, by the direct

inducements which it holds out to the maintenance of a character for

industry, integrity and prudence."

The result was that the Scottish banks were allowed

to keep their note issues. But this enquiry also lent considerable

weight to Joplin's argument and legislators in London became

increasingly aware of the Scottish system of banking and its successes

compared with the English system and its weaknesses.

In Ireland too, where the system had emerged like

that of England, with a monopolistic Bank of Ireland in Dublin and a

series of small country banks, there had developed pressure for change.

Several pieces of legislation between 1824 and 1833 gradually removed

the restrictive legislation in Ireland and England and enabled these

countries to develop banking systems on the Scottish model. In this way

began a general exodus of Scottish bankers into other parts of the

British Isles and eventually to other parts of the world.

Pressure for change had built up in England and

Ireland as a result of developments in the economy and this pressure was

also manifest in Scotland. It was a period of considerable growth and

large scale developments in building, iron steamships and railways

placed increasing demands upon the banking system. The result of this

pressure was that the provincial banking companies were replaced by a

series of joint-stock banks. These new arrivals were very similar to the

provincial banking companies but differed from them in the important

respect that they were very much bigger. They had a larger capital base

and whereas the provincial banks usually had only local branch networks

many of the new joint-stock banks developed banking systems which were

national in scope and which soon came to rival the Edinburgh banks.

Several of these new joint-stock banks like the Commercial Bank of

Scotland and National Bank of Scotland were Edinburgh-based while others

were based in the other major cities, e.g., the Glasgow Union

Bank (later Union Bank of Scotland) and Clydesdale Bank in Glasgow, and

the North of Scotland Bank in Aberdeen. These joint-stock banks and the

Edinburgh banks gradually took over the provincial banks until by 1864

when the Royal Bank took over the Dundee Banking Company only the

joint-stock banks and the three Edinburgh public banks remained. By this

time both the Commercial Bank and the National Bank had obtained Royal

Charters but neither had managed to obtain the privilege of limited

liability which remained the prerogative of the three oldest Scottish

banks.

Such had been the success of the Scottish banking

system that many writers attributed to the banks a large portion of the

credit for the rapid development of the Scottish economy. From being a

poor neighbour of England in 1750, Scotland had, a century later, a

national income per capita which was probably at least the equal

of England's. Numerous factors were of course responsible for this and

the extent to which the Scots had evolved a banking system which

pioneered in so many ways is a sure indicator of the importance of

banking to the development of the economy.

One other aspect of this development was the Savings

Bank movement which began in a very small way at Ruthwell in

Dumfriesshire in 1810 when the Rev. Henry Duncan founded a parish

savings bank. The idea was basically to gather the savings of the poorer

classes of society and to deposit them en bloc in one or other of

the commercial banks who, being keen to encourage the savings movement,

offered a slightly higher rate of interest than was normal on deposits.

The movement spread rapidly throughout the British Isles. Under Acts of

1817 and 1828 English Savings Banks were enabled to invest their funds

in Government Securities. By an Act of 1835 this facility was extended

to Scotland. Banks which registered under this Act (e.g., the

Savings Bank of Glasgow) became Trustee Savings Banks, i.e.,

their management was vested in a board of trustees. Savings banks placed

their funds between the commercial banks and the Government.

There was from then on a complementarity between the

savings banks on the one hand and the commercial banks on the other. One

result of this was that the latter seldom attracted deposits direct from

those parts of society below the middle class income range. This

situation prevailed for over 100 years.

All of these new developments in banking, however,

were not achieved without some difficulty. In the 1830s and early 1840s

there were a number of failures of joint-stock banks in England and, in

addition to this, it was a period which experienced several commercial

crises and some inflation. The Government blamed the banks for

destabilising the economy by creating too much credit and for a number

of years a great debate ran its course between the Government and its

supporters (Currency school) on the one hand and the bankers (Banking

school) on the other. The bankers believed that so long as each credit

they extended was to meet the legitimate needs of trade then there could

be no inflation. The debate itself was rather inconclusive but in 1844

the Government acted on its beliefs and passed the Bank Charter Act

which was intended to limit the growth—particularly the note issues—of

the banks. The Act separated the banking and note issuing functions of

the Bank of England and tied the note issue to the supply of gold in the

country; in effect to the balance of payments. As far as joint-stock

banks (in England and Wales) were concerned no new bank could have a

note issue and existing issues were to be limited to the average of

their issues over a three-month period in 1844. If any banks merged or

opened an office in London they were to lose their note issue. These

last provisions were critical for eventually all banks came into one or

other of these categories and so lost their note issues. In this way the

Bank of England eventually gained a monopoly of all note issues in

England and Wales.

Similar legislation was proposed for Scotland and

Ireland but such was the outcry from these countries that they were

treated differently. The note issues were limited to the average of the

year preceding the passing of the Act in 1845 and any excess issue

beyond these authorised limits had to be backed by gold. The Scottish

and Irish banks were not however forced to lose their issue if they

merged with another bank or opened a London office. The result of this

has been that both Scottish and Irish banks have retained their rights

to issue notes to the present day. (Irish banks, of course, now only

issue in Northern Ireland.)

The legislation had the desired effect of limiting

the ability of all banks in the British Isles to issue notes but it did

not cure the problem of instability and inflation. Indeed the Act of

1844 had to be relaxed in the crises of 1847, 1857 and 1866. The

difficulty was that the banks had begun to develop payments by cheque

thus obviating the need for bank-notes, i.e., deposits and

deposit creation were becoming more important as bank liabilities than

notes. The legislation had not taken account of this development.

In the second half of the 19th century the banks

concentrated increasingly on attracting deposits and it was generally a

period of substantial growth in the economy and in banking. In the

period between 1850 and 1873 Britain can be said to have been the

"Workshop of the World" and although there were difficulties after 1873,

as other countries began to industrialise behind substantial tariff

barriers, it was nevertheless an era of development especially in

Scotland which experienced the growth of much of the heavy industry,

including shipbuilding, for which the country became so famous.

This growth in the scale of industry and trade posed

challenges to the banking system. The major challenge was that

individual customers now required more substantial advances from their

bankers than had been normal in the past. Most banks appear to have met

this challenge in a highly effective way although this is an area in

which much research requires to be done so that we may learn more about

the techniques of lending.

There was, however, one notable failure to meet this

challenge and this was the City of Glasgow Bank. This concern had become

too heavily committed to a few firms most of which were owned by the

Directors of the Bank. In a desperate effort to extricate themselves

from their difficulties the Directors had begun to falsify the accounts

but this was all to no avail and the Bank failed in 1878.

The liability of the shareholders was unlimited and

several calls were made upon them to pay the debts of the Bank. Only 254

of the 1,819 shareholders remained solvent when the affairs of the Bank

were finally wound up. All the creditors were paid in full.

The failure of the City of Glasgow Bank was a severe

jolt to the confidence and self esteem of the rest of the Scottish

banking system but the bankers were quick to learn the lessons and took

steps to prevent the possibility of such a disaster ever happening

again. Within a very short space of time after the closure the other

banks had moved to have their shareholders appoint auditors who would

report annually on the state of the accounts. This was the origin of

independent auditing and acted as a control by the shareholders on the

intromissions of the Directors.

A more vexed question was that concerning the

liability of the shareholders for the debts of their bank. Many believed

that unlimited liability was a good thing and that to limit liability

would be damaging to a bank's image. This view ignored the fact that the

three oldest banks had always had limited liability. Such was the fear

engendered by the failure of 1878, however, that most banks favoured the

view that limitation of liability was in the best interests of their

shareholders. All seven unlimited banks registered with limited

liability and added "limited" to their names from 1882. The principle of

limited liability had been available to bankers generally since 1862.

In England and Wales banks met the challenge of

increased demands from customers with a merger movement. There were

numerous amalgamations amongst banks in the late 19th century and one

result of a merger of several banks was the emergence of Barclays Bank

in the 1890s.

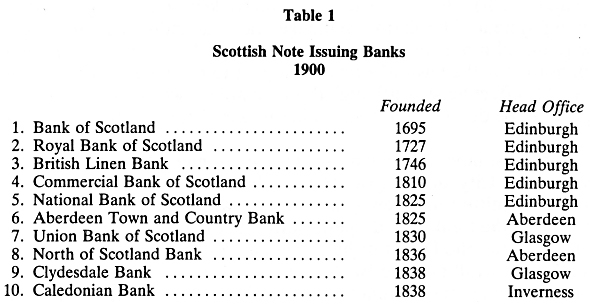

There was limited scope for further mergers in

Scotland where the average bank was still larger than its English

counterpart. At the dawn of the 20th century there were ten note-issuing

banks north of the border and an as yet unquantified number of savings

banks. The note issuers were:

This was not, however, a stable situation for in

1907-8 the Caledonian Bank was taken over by the Bank of Scotland. Also

in 1907 the two Aberdeen banks amalgamated. Meanwhile in England the

merger movement continued apace and some of the, by now very large,

banks began to look outside England for acquisitions.

The first success in this sphere was the purchase in

1918 of the shares of the National Bank of Scotland by Lloyds Bank

although the arrangement that the two banks were to maintain separate

identities was to characterise this type of activity. By this time of

course the average Scottish bank was much smaller than any of the

English "Big Five". The Scots were therefore vulnerable to takeover bids

and some actively encouraged them seeing advantages in economies of

scale from an affiliation with an English clearing bank. In 1919

Barclays Bank acquired the share capital of the British Linen Bank and

the Clydesdale was acquired by the Midland Bank which also purchased the

North of Scotland Bank in 1923.

The Scots were not without their responses to this

movement and in 1924 the Royal Bank acquired the small but prestigious

Drummond's Bank which retains its very singular identity. This was

followed in 1930 by the acquisition of Williams Deacons Bank, based in

the north-west of England, and in 1939 by Glyn, Mills Bank which was

based in London and the south-east of England. Drummond's was

assimilated into the Royal Bank but the other two retained their

identities forming, with the Royal, the "Three Banks Group". The Royal

also took over the London West End branch of the Bank of England in

1930.

By 1939 there were eight Scottish banks—four

independent and four "affiliated" with English banks. In the post-war

years the pressure for rationalisation and economies of scale dictated

the need of further mergers, as it had in other sectors of the economy.

In 1950 the Midland Bank merged its two Scottish banks to form the

Clydesdale and North of Scotland Bank (later abbreviated to Clydesdale

Bank). Agreement on a merger was reached between the Bank of Scotland

and Union Bank in 1952. In 1958 the Commercial Bank and National Banks

merged, with Lloyds Bank (owners of the National) getting a 37 per cent

stake in the new National Commercial Bank of Scotland which immediately

became the largest Scottish bank.

In the late 1960s mergers again became fashionable.

The National Commercial Bank absorbed the thirty-six English branches of

the Irish-based National Bank in 1966. In 1969 it was announced that the

Royal and the National Commercial were to merge. The English

subsidiaries Williams, Deacons and Glyn, Mills were then merged to form

Williams and Glyns Bank.

Also in 1969 the union was announced between the Bank

of Scotland and the British Linen, with Barclays Bank (owners of the

British Linen) taking a 35 per cent stake in the new Bank of Scotland.

By then the Scottish banking system was reduced to three banks—Bank of

Scotland, Royal Bank of Scotland and Clydesdale Bank.

The last twenty years have also been a period of

rapid change in other areas of banking. In the mid-1960s the Trustee

Savings Banks decided that they would expand their business beyond the

traditional savings and investment accounts by offering current accounts

with chequeing facilities and encouraging people to have salaries paid

into these accounts as was already the practice in the commercial banks.

This development was obviously designed to make the Trustee Savings

Banks more competitive with the commercial banks for the business of

personal account customers. It was a move which foreshadowed the

developments of the 1970s.

The Committee to review National Savings reported in

1973. The recommendations of the Page Report expressed the view that the

Trustee Savings Banks should be permitted to develop as a "third force"

in British banking and since then the T.S.Bs have taken several steps to

expand their services. A Central Trustee Savings Bank was set up in 1973

to co-ordinate and control activities and in 1976 application was made

to join the London Bankers Clearing House. Most of the banks have merged

with some of their neighbours so that there are now eighteen regional

T.S.Bs in Britain. Since then the T.S.Bs have gradually shaken off their

close contacts with Government and have been integrated into the

commercial banking sector under the supervision of the Bank of England.

In 1982 the four Scottish T.S.Bs established a

Steering Committee to manage the arrangements for a merger of the four

banks with effect from May 1983—the new bank to be called T.S.B.

Scotland.

Just as competition for the commercial banks has

emerged from a source which was once complementary to their operation so

it has also emerged from organisations entirely new to Scotland.

Merchant banks specialising in portfolio management and corporate

financial services had long been a feature of the London financial

scene. Several London-based merchant banks opened Scottish offices in

the late 1960s and early 1970s and there was also some Scottish

initiative—notably Noble, Grossart in 1969. Some of these new arrivals

were shaken out in the banking crisis of 1973-4 and retired to their

London base but others remained to provide a range of services which

were both competitive with and complementary to those provided by the

commercial banks. Co-operation was particularly marked in the area of

North Sea Oil finance.

Competition also came from the finance companies—some

of whom had been in existence from the inter-war years but the network

of offices expanded greatly in the 1960s and 1970s. It came too,

although only in a limited way, from branches of overseas banks and the

English clearing banks establishing offices in Scotland.

Beyond the banking sector was the non-bank financial

sector including the building societies, insurance companies, investment

trusts and national savings. All of these had been around for a long

time but changes in policy dictated that all should be more competitive

in the search for deposit and investment money. This meant more

competition for the banks. The age of competition was fostered by the

Bank of England when in 1971 it published "Competition and Credit

Control".

The banks responded to this new surge of competition

by buying up controlling interests in finance houses and hire purchase

companies and by setting up their own merchant bank subsidiaries. It was

not of course possible to buy up building societies but banks met the

competition by themselves offering mortgages at increasingly competitive

rates.

In short the period from about 1955 to the present

was one which presented a whole new range of challenges to the banking

system. An editorial in the Bankers Magazine in 1976 concluded

that—

"this phase in our economic history offers a

challenge as great, and in its way as exhilarating as that provided

by the breakthrough in our industrial revolution."

The result was a series of changes of outlook,

structure and function in the banking system which was just as dramatic

as that which occurred during the industrial revolution. Yet the

consequences for the economy could be even greater, for the challenge

which faced the bankers 150 years ago was of how to finance a buoyant

and expanding economy whilst that which faces the banker today is the

much more difficult problem of how to prevent secular decline and put

the economy back on an even growth path.